How Traditional Whole Life Insurance Works

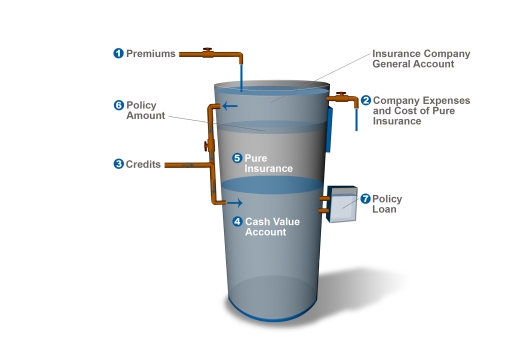

- The premium you "pour in" is fixed for the life of the policy. As you age, the cost of insuring your life increases. However, your premium stays the same, because the company projects this expense in advance and factors it into the premium at the onset.

- As you pay your premium, the insurance company deducts all of its expenses, premium taxes, and the cost of pure insurance (net amount of risk coverage), or mortality charge.

- The remainder of your premium represents a portion of the insurance company's investment portfolio. Your cash value account is credited with a fixed amount (predetermined by your contract) at the end of each premium period.

- Like water in a tank, the level of your cash value rises over time.

- As the cash value increases, the amount of risk coverage (or pure insurance) in the policy decreases.

- When you die, your beneficiary receives the "full tank" of the policy amount, which is the sum of the cash value and the pure insurance.

- You may take a policy loan in an amount not to exceed the policy's cash surrender value less the annual loan interest. Repayment replenishes your cash value, but there may be a tax liability if the policy terminates before the death of the insured. Any loan balance outstanding (plus interest due) at the time of your death would be deducted from the policy amount.

**This is a Forefield 3rd party article which is being submitted by Wealth Strategies Financial Group.

Copyright 2018 Broadridge Advisor Solutions